Consumer-Directed Health Care for Persons Under 65 Years of Age with Private Health Insurance: United States, 2007

- Key findings

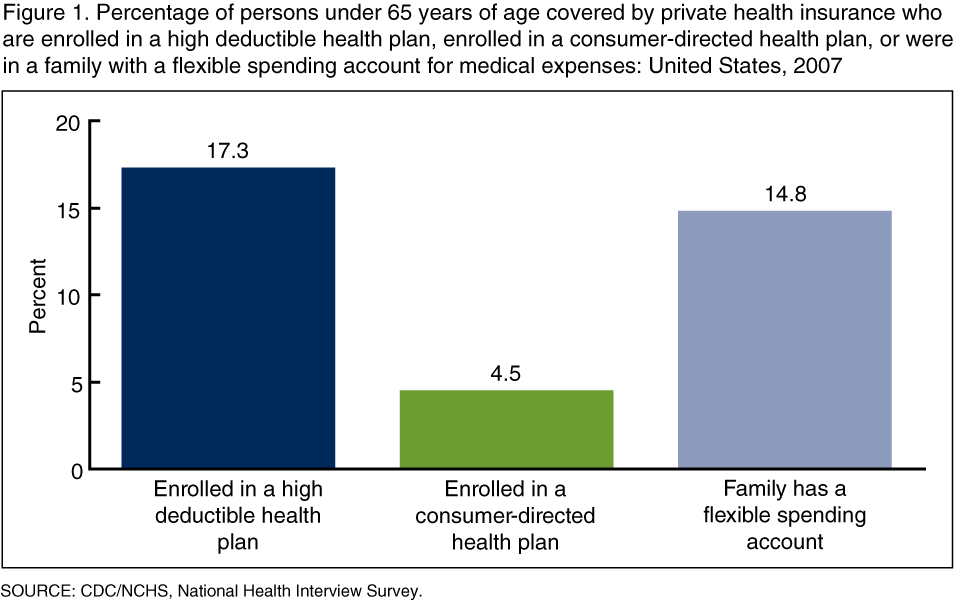

- In 2007, 17.3% of persons under 65 years of age with private health insurance were enrolled in a HDHP, 4.5% were enrolled in a CDHP, and 14.8% were in a family with a FSA for medical expenses.

- Persons with directly purchased private health plans were more likely to be enrolled in a HDHP than those with employment-based coverage.

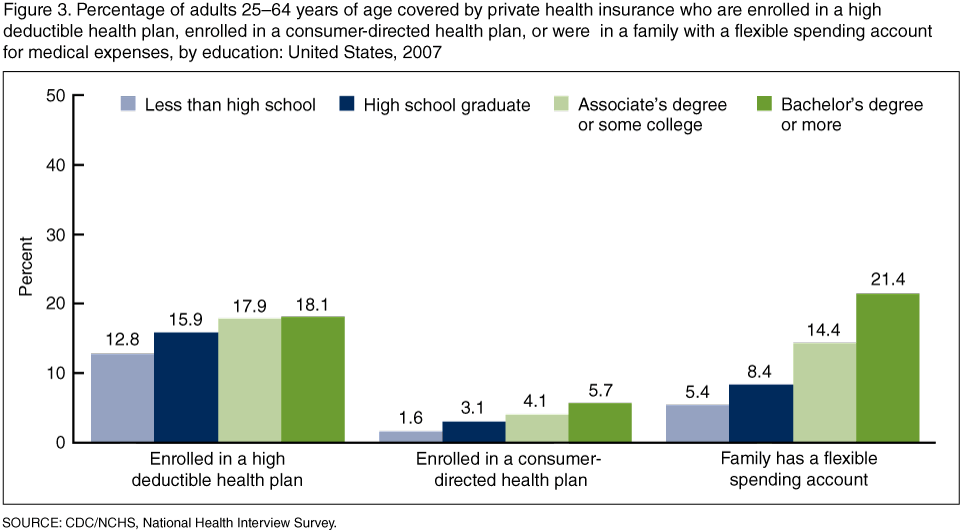

- Higher educational attainment was associated with higher rates of enrollment in consumer-directed health care options.

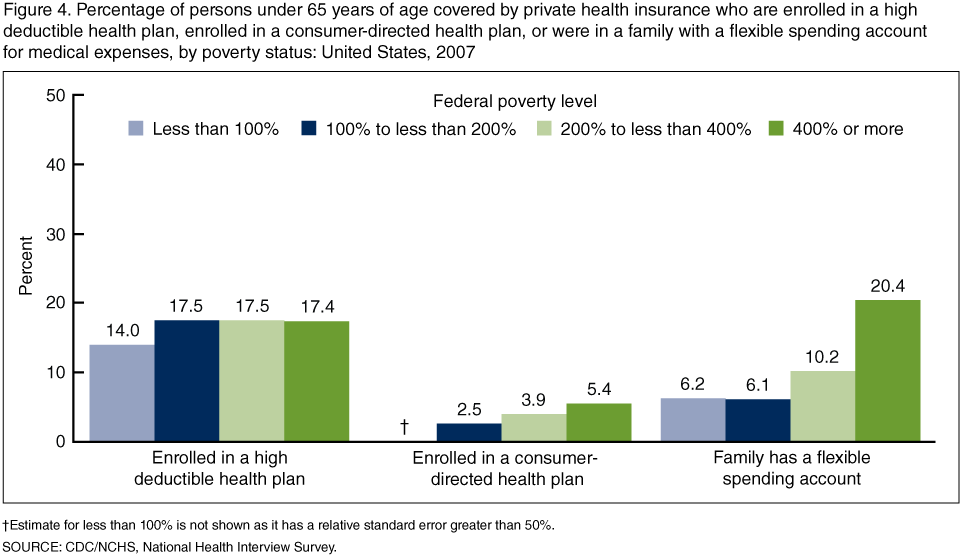

- Rates of enrollment increased with higher incomes for CDHPs and FSAs but not for HDHPs.

- Summary

- Definitions

- Data source and methods

- About the authors

- References

- Suggested citation

NCHS Data Brief No. 15, March 2009

PDF Versionpdf icon (998 KB)

by Robin A. Cohen, Ph.D., and Michael E. Martinez, M.P.H.

Key findings

Data from the National Health Interview Survey

- In 2007, 17.3% of persons under 65 years of age with private health insurance were enrolled in a high deductible health plan (HDHP), 4.5% were enrolled in a consumer-directed health plan (CDHP), and 14.8% were in a family with a flexible spending account for medical expenses (FSA).

- Persons with directly purchased private health insurance were more likely to be enrolled in a high deductible plan than those who obtained their private health insurance through an employer or union.

- Higher incomes and higher educational attainment were associated with greater uptake and enrollment in HDHPs, CDHPs, and FSAs.

National attention to consumer-directed health care has increased following the enactment of the Medicare Prescription Drug Improvement and Modernization Act of 2003 (P.L. 108-173), which established tax-advantaged health savings accounts (1). Consumer-directed health care enables individuals to have more control over when and how they access care, what types of care they use, and how much they spend on health care services. This report includes estimates of three measures of consumer-directed private health care. Estimates for 2007 are provided for enrollment in high deductible health plans (HDHPs), plans with high deductibles coupled with health savings accounts also known as consumer-directed health plans (CDHPs), and the percentage of individuals with private coverage whose family has a flexible spending account (FSA) for medical expenses, by selected sociodemographic characteristics.

Keywords: Private health insurance, high deductible plan, consumer-directed plan, flexible spending account, National Health Interview Survey

In 2007, 17.3% of persons under 65 years of age with private health insurance were enrolled in a HDHP, 4.5% were enrolled in a CDHP, and 14.8% were in a family with a FSA for medical expenses.

image icon

image icon

Children under 18 years of age (16.2%) with private health insurance were more likely to be in a family with a FSA for medical expenses than adults aged 18-64 years (14.4%) with private health insurance (See table).

There were no significant differences between males and females with private health insurance with respect to enrollment in a HDHP, enrollment in a CDHP, or being in a family with a FSA for medical expenses.

Hispanic and non-Hispanic black persons under 65 years of age with private health insurance were less likely to be enrolled in a HDHP and were less likely be in a family with a FSA for medical expenses than non-Hispanic white, non-Hispanic Asian, and other non-Hispanic persons with private health insurance.

Non-Hispanic white persons under 65 years of age with private health insurance were more than twice as likely to be enrolled in a CDHP as Hispanic and non-Hispanic black persons under 65 years of age with private health insurance.

Persons with directly purchased private health plans were more likely to be enrolled in a HDHP than those with employment-based coverage.

Of persons under 65 years of age with directly purchased private health insurance, 40% were enrolled in a HDHP compared with about 15% of persons under 65 years of age with employer based private health insurance.

image icon

image icon

Enrollment in CDHPs did not vary by source of private coverage.

Persons under 65 years of age with employer-based private health insurance were over three times as likely to be in a family with a FSA as persons 65 years of age and under with directly purchased health insurance.

Table 1a. Percentage of persons under 65 years of age covered by private health insurance who are enrolled in a high deductible health plan, enrolled in a consumer-directed health plan, or in a family with a flexible spending account for medical expenses, by age: United States, 2007

| Age | Enrolled in a high deductible plan1 | Enrolled in a consumer-directed health plan2 | Family has a flexible spending account3 |

|---|---|---|---|

| Percent (standard error) | |||

| Under 65 years | 17.3 (0.45) | 4.5 (0.28) | 14.8 (0.39) |

| Under 18 years | 18.3 (0.68) | 5.0 (0.42) | 16.2 (0.61) |

| 18-64 years | 16.9 (0.43) | 4.3 (0.28) | 14.4 (0.38) |

See footnotes at end of Table 1h.

Table 1b. Percentage of persons under 65 years of age covered by private health insurance who are enrolled in a high deductible health plan, enrolled in a consumer-directed health plan, or in a family with a flexible spending account for medical expenses, by sex: United States, 2007

| Sex | Enrolled in a high deductible plan1 | Enrolled in a consumer-directed health plan2 | Family has a flexible spending account3 |

|---|---|---|---|

| Percent (standard error) | |||

| Male | 17.7 (0.51) | 4.5 (0.29) | 14.5 (0.41) |

| Female | 16.9 (0.47) | 4.4 (0.32) | 15.2 (0.42) |

See footnotes at end of Table 1h.

Table 1c. Percentage of persons under 65 years of age covered by private health insurance who are enrolled in a high deductible health plan, enrolled in a consumer-directed health plan, or in a family with a flexible spending account for medical expenses, by Hispanic origin and race: United States, 2007

| Hispanic origin and race | Enrolled in a high deductible plan1 | Enrolled in a consumer-directed health plan2 | Family has a flexible spending account3 |

|---|---|---|---|

| Percent (standard error) | |||

| Hispanic | 13.5 (0.99) | 2.3 (0.45) | 9.6 (0.73) |

| Non-Hispanic white | 18.3 (0.54) | 5.1 (0.37) | 16.5 (0.49) |

| Non-Hispanic black | 13.2 (1.03) | 2.1 (0.40) | 8.0 (0.69) |

| Non-Hispanic Asian | 17.6 (1.82) | 3.8 (0.79) | 15.4 (1.48) |

| Non-Hispanic other | 19.1 (2.64) | *3.9 (1.35) | 13.9 (2.01) |

See footnotes at end of Table 1h.

Table 1d. Percentage of persons under 65 years of age covered by private health insurance who are enrolled in a high deductible health plan, enrolled in a consumer-directed health plan, or in a family with a flexible spending account for medical expenses, by education: United States, 2007

| Education4 | Enrolled in a high deductible plan1 | Enrolled in a consumer-directed health plan2 | Family has a flexible spending account3 |

|---|---|---|---|

| Percent (standard error) | |||

| Less than a high school diploma | 12.8 (1.06) | 1.6 (0.45) | 5.4 (0.65) |

| High school graduate | 15.9 (0.68) | 3.1 (0.34) | 8.4 (0.45) |

| Associate’s degree or some college | 17.9 (0.65) | 4.1 (0.34) | 14.4 (0.59) |

| Bachelor’s degree or more | 18.1 (0.62) | 5.7 (0.39) | 21.4 (0.63) |

See footnotes at end of Table 1h.

Table 1e. Percentage of persons under 65 years of age covered by private health insurance who are enrolled in a high deductible health plan, enrolled in a consumer-directed health plan, or in a family with a flexible spending account for medical expenses, by employment status: United States, 2007

| Employment status5 | Enrolled in a high deductible plan1 | Enrolled in a consumer-directed health plan2 | Family has a flexible spending account3 |

|---|---|---|---|

| Percent (standard error) | |||

| Employed | 16.5 (0.43) | 4.3 (0.28) | 15.4 (0.41) |

| Unemployed | 25.0 (2.95) | 7.2 (1.79) | 9.7 (1.78) |

| Not in workforce | 19.0 (0.81) | 3.9 (0.44) | 9.6 (0.51) |

See footnotes at end of Table 1h.

Table 1f. Percentage of persons under 65 years of age covered by private health insurance who are enrolled in a high deductible health plan, enrolled in a consumer-directed health plan, or in a family with a flexible spending account for medical expenses, by marital status: United States, 2007

| Marital status4 | Enrolled in a high deductible plan1 | Enrolled in a consumer-directed health plan2 | Family has a flexible spending account3 |

|---|---|---|---|

| Percent (standard error) | |||

| Married | 17.5 (0.50) | 4.6 (0.27) | 16.0 (0.47) |

| Widowed | 17.5 (2.41) | 4.8 (1.34) | 7.8 (1.51) |

| Divorced or separated | 16.9 (0.98) | 3.9 (0.63) | 11.6 (0.70) |

| Living with a partner | 15.2 (1.58) | 4.2 (1.14) | 13.1 (1.43) |

| Never married | 15.3 (1.04) | 2.9 (0.44) | 12.0 (0.75) |

See footnotes at end of Table 1h.

Table 1g. Percentage of persons under 65 years of age covered by private health insurance who are enrolled in a high deductible health plan, enrolled in a consumer-directed health plan, or in a family with a flexible spending account for medical expenses, by poverty status: United States, 2007

| Poverty status6 | Enrolled in a high deductible plan1 | Enrolled in a consumer-directed health plan2 | Family has a flexible spending account3 |

|---|---|---|---|

| Percent (standard error) | |||

| Less than 100% | 14.0 (2.08) | † | 6.2 (1.03) |

| 100%-less than 200% | 17.5 (1.44) | 2.5 (0.60) | 6.1 (0.73) |

| 200%-less than 400% | 17.5 (0.78) | 3.9 (0.41) | 10.2 (0.58) |

| 400% and more | 17.4 (0.64) | 5.4 (0.42) | 20.4 (0.60) |

See footnotes at end of Table 1h.

Table 1h. Percentage of persons under 65 years of age covered by private health insurance who are enrolled in a high deductible health plan, enrolled in a consumer-directed health plan, or in a family with a flexible spending account for medical expenses, by source of private health insurance plan: United States, 2007

| Source of private health insurance plan | Enrolled in a high deductible plan1 | Enrolled in a consumer-directed health plan2 | Family has a flexible spending account3 |

|---|---|---|---|

| Percent (standard error) | |||

| Employer-based coverage | 15.4 (0.44) | 4.4 (0.30) | 15.7 (0.42) |

| Directly purchased | 40.0 (1.81) | 5.3 (0.93) | 4.7 (0.71) |

*Estimates preceded by an (*) have a relative standard error greater than 30% and less than or equal to 50% and should be used with caution as they do not meet the standard of reliability or precision.

†Estimates with a relative standard error of greater than 50% are replaced with a dagger and are not shown.

1A high deductible health plan (HDHP) was defined as a private health plan with an annual deductible of not less than $1,100 for self-only coverage or $2,200 for family coverage.

2Consumer-directed health plan (CDHP) was defined as a HDHP with a special account to pay for medical expenses; unspent funds are carried over to subsequent years. A person was considered to have a CDHP if there was a “yes” response to the following question: “With this plan, is there a special account or fund that can be used to pay for medical expenses? The accounts are sometimes referred to as Health Savings Accounts (HSAs), Health Reimbursement Accounts (HRAs), Personal Care Accounts, Personal medical funds, or Choice funds, and are different from Flexible Spending Accounts.”

3A person was considered to be in a family with a flexible spending account (FSA) for medical expenses if there was a “yes” response to the following question: “Do you or anyone in your family have a Flexible Spending Account for health expenses? These accounts are offered by some employers to allow employees to set-aside pre-tax dollars of their own money for their use throughout the year to reimburse themselves for their out-of-pocket expenses for health care. With this type of account, any money remaining in the account at the end of the year, following a short grace period, is lost to the employee.” Persons who were covered by a CDHP and were also in a family with a FSA were considered not to be covered by a FSA.

4Education and marital status are shown only for persons 25-64 years of age.

5Employment status is shown only for persons 18-64 years of age.

6Poverty status is based on family income and family size using the U.S. Census Bureau’s poverty thresholds. Estimates by poverty status are based on both reported and imputed family income. Family income information was completely missing for 10.6% of persons, and family income information was only reported in broad categories for an additional 23.6% of persons in 2007. Therefore, family income was imputed for 34.2% of persons in 2007 using NHIS imputed income files.

SOURCE: Family Core component of the 2007 National Health Interview Survey (NHIS). Data are based on household interviews of a sample of the civilian noninstitutionalized population.

Higher educational attainment was associated with higher rates of enrollment in consumer-directed health care options.

Among adults 25-64 years of age with private coverage, 17.9% with an Associate’s degree or some college and 18.1% with at least a Bachelor’s degree were enrolled in a HDHP compared with 12.8% with less than a high school education and 15.9% who only graduated from high school.

image icon

image icon

Enrollment in a CDHP or being in a family with a FSA increased with increased educational attainment. Among adults 25-64 years of age with private coverage and an education of a bachelor’s degree or more, almost 6% were enrolled in a CDHP and over 21% were in a family with a FSA.

Rates of enrollment increased with higher incomes for CDHPs and FSAs but not for HDHPs.

Enrollment in a HDHP did not vary by family income.

In 2007, 5.4% of persons under 65 years of age with private health insurance and with family incomes at or above 400% of the federal poverty level (FPL) were enrolled in a CDHP compared with 2.5% of persons whose family income was 100% to less than 200% of the FPL.

More than 20% of persons under 65 years of age with private health insurance and a family income at or above 400% of the FPL were in a family with a FSA. In contrast, approximately 6% of persons under 65 years of age with private health insurance and a family income below 200% of the FPL were in a family with a FSA.

image icon

image icon

Summary

Sociodemographic and socioeconomic factors were associated with consumer-directed health care (See table). Age and race were associated with enrollment in a HDHP, enrollment in a CDHP, and being in a family with a FSA. Married adults were more likely to be in a family with a FSA than nonmarried adults. Employed adults and persons with employer sponsored private health insurance were less likely to be enrolled in a HDHP than other adults. More highly educated and affluent persons were more likely to be enrolled in a CDHP than those who were less educated and had lower family incomes.

Definitions

Private insurance: Is indicated when respondents report that they were covered at the time of the interview by private health insurance through an employer or union, or if they purchased a policy on their own. Private health insurance includes managed care such as health maintenance organizations (HMOs). It does not include military health plans.

High deductible health plan (HDHP): Private health plan with an annual deductible of not less than $1,100 for self-only coverage or $2,200 for family coverage for 2007.

Consumer-directed health plan (CDHP): A HDHP with a special account to pay for medical expenses; unspent funds are carried over to subsequent years. A person is considered to have a CDHP if there was a “yes” response to the following question: “With this plan, is there a special account or fund that can be used to pay for medical expenses? The accounts are sometimes referred to as Health Savings Accounts (HSAs), Health Reimbursement Accounts (HRAs), Personal Care Accounts, Personal medical funds, or Choice funds, and are different from Flexible Spending Accounts.”

Flexible spending account (FSA): Accounts that are offered by some employers to allow employees to set-aside pre-tax dollars of their own money for their use throughout the year to reimburse themselves for their out-of-pocket expenses for health care. For this type of account, any money remaining in the account at the end of the year, following a short grace period, is lost to the employee. A person was considered to be covered by a FSA based on a “yes” response to the question “Do you or anyone in your family have a Flexible Spending Account for health expenses? These accounts are offered by some employers to allow employees to set-aside pre-tax dollars of their own money for their use throughout the year to reimburse themselves for their out-of-pocket expenses for health care. With this type of account, any money remaining in the account at the end of the year, following a short grace period, is lost to the employee.” Persons who were covered by a CDHP and were also in a family with a FSA were considered not to be covered by a FSA.

Poverty status or percentage of poverty level: Is based on family income, family size, and the number of children in the family, and, for families with two or fewer adults, on the age of the adults in the family. The poverty level is based on definitions originally developed by the Social Security Administration. These include a set of income thresholds that vary by family size and composition. Families or individuals with income below their appropriate thresholds are classified as below the poverty level. These thresholds are updated annually by the U.S. Census Bureau to reflect changes in the Consumer Price Index for all urban consumers (CPI U) (2). Estimates by poverty status are based on both reported and imputed family income. Family income information was completely missing for 10.6% of persons, and family income information was only reported in broad categories for an additional 23.6% of persons in 2007. Therefore, family income was imputed for 34.2% of persons in 2007 using NHIS imputed income files (3).

Data source and methods

Data from the 2007 NHIS were used for this analysis. NHIS collects information about the health and health care of the civilian noninstitutionalized population of the United States. Interviews are conducted in the respondents’ households primarily, but follow ups in order to complete interviews may be conducted over the telephone. Only persons under 65 years of age with private health insurance were included in this analysis. The questions about HDHPs, CDHPs, and FSAs were first included in the 2007 NHIS. Detailed questions about private health insurance plans are asked on a plan basis. Information is collected on up to four private health insurance plans per family. Questions about HDHPs and CDHPs were asked for each private health insurance plan. The question about FSAs was asked on a family basis and includes all persons in the family without regard to insurance status. Only persons with private health insurance were included in this analysis. In 2007, 67,325 persons under age 65 were included in the Family Core component on the NHIS.

NHIS is designed to yield a nationally representative sample, and this analysis uses weights to produce national estimates. Data weighting procedures are described in more detail elsewhere (4) (NHIS Methods). Point estimates and estimates of corresponding variances for this analysis were calculated using the SUDAAN software package (5) to account for the complex sample design of the NHIS. The Taylor series linearization method was chosen for variance estimation. All estimates shown meet the National Center for Health Statistics (NCHS) standard for having a relative standard error less than or equal to 30%. Differences between percentages were evaluated using two-sided significance tests at the 0.05 level. Terms such as “similar” and “no difference” indicate that the statistics being compared were not significantly different. Lack of comment regarding the difference between any two statistics does not necessarily suggest that the difference was tested and found to not be significant. NHIS is conducted continuously throughout the year by interviewers of the U.S. Census Bureau for the Centers for Disease Control and Prevention’s NCHS. For further information about NHIS see the NCHS website at: NHIS homepage.

About the authors

Robin A. Cohen and Michael E. Martinez are with the Centers for Disease Control and Prevention’s National Center for Health Statistics, Division of Health Interview Statistics.

References

- United States Government Accountability Office. Consumer-directed health plans: Early enrollee experiences with health savings accounts and eligible health plans. GAO-06-798. Washington. 2006.

- DeNavas-Walt C, Proctor BD, Smith J. U.S. Census Bureau. Current population reports, P60-233, Income, poverty, and health insurance coverage in the United States, 2006 pdf icon[PDF – 3 MB]external icon. U.S. Government Printing Office, Washington, DC. 2007.

- Schenker N, Raghunathan TE, Chiu P, Makuc DM, Zhang G, Cohen AJ. Multiple imputation of family income and personal earnings in the National Health Interview Survey: Methods and examples pdf icon[PDF – 813 KB].

- Botman SL, Moore TF, Moriarity CL, Parsons VL. Design and estimation for the National Health Interview Survey, 1995-2004. National Center for Health Statistics. Vital Health Stat 2(130). 2000.

- Research Triangle Institute. SUDAAN (Release 9.1). Research Triangle Park, NC: Research 5. Triangle Institute. 2004.

Suggested citation

Cohen RA, Martinez, ME. Consumer-directed health care for persons under 65 years of age with private health insurance: United States, 2007. NCHS data brief, no 15. Hyattsville, MD: National Center for Health Statistics. 2009.

Copyright information

All material appearing in this report is in the public domain and may be reproduced or copied without permission; citation as to source, however, is appreciated.

National Center for Health Statistics Director

Edward J. Sondik, Ph.D.

Acting Co-Deputy Directors

Jennifer H. Madans, Ph.D.

Michael H. Sadagursky